Regulation E Bank Fraud Playbook: Protect Cash Flow After Unauthorized Transfers

A practical, source-backed checklist for responding to unauthorized debit, ACH, ATM, and payment-app transfers without losing control of rent, bills, and emergency cash.

Unauthorized transfers create two problems at once: a consumer-protection problem and a cash-flow problem. The protection problem is about Regulation E, bank investigation duties, identity-theft reports, and written disputes. The cash-flow problem is more immediate: rent is still due, a debit card may be frozen, autopay bills may bounce, and a provisional credit can be reversed if the institution later decides against you. This playbook is designed to help you respond fast without accidentally treating uncertain money as spendable.

Latest review: May 25, 2026. This article uses public guidance from the CFPB, FTC, FDIC, Federal Reserve, and the current eCFR version of Regulation E. It is educational information, not legal, tax, or individualized financial advice.

First, identify what kind of money movement happened

Regulation E generally applies to electronic fund transfers involving consumer accounts, such as debit-card transactions, ATM withdrawals, ACH transfers, and many recurring electronic payments. That does not mean every painful loss is automatically reimbursed. A debit-card charge you never authorized is different from a payment you intentionally sent to a scammer, and both are different from a check, wire transfer, credit-card transaction, or merchant refund dispute.

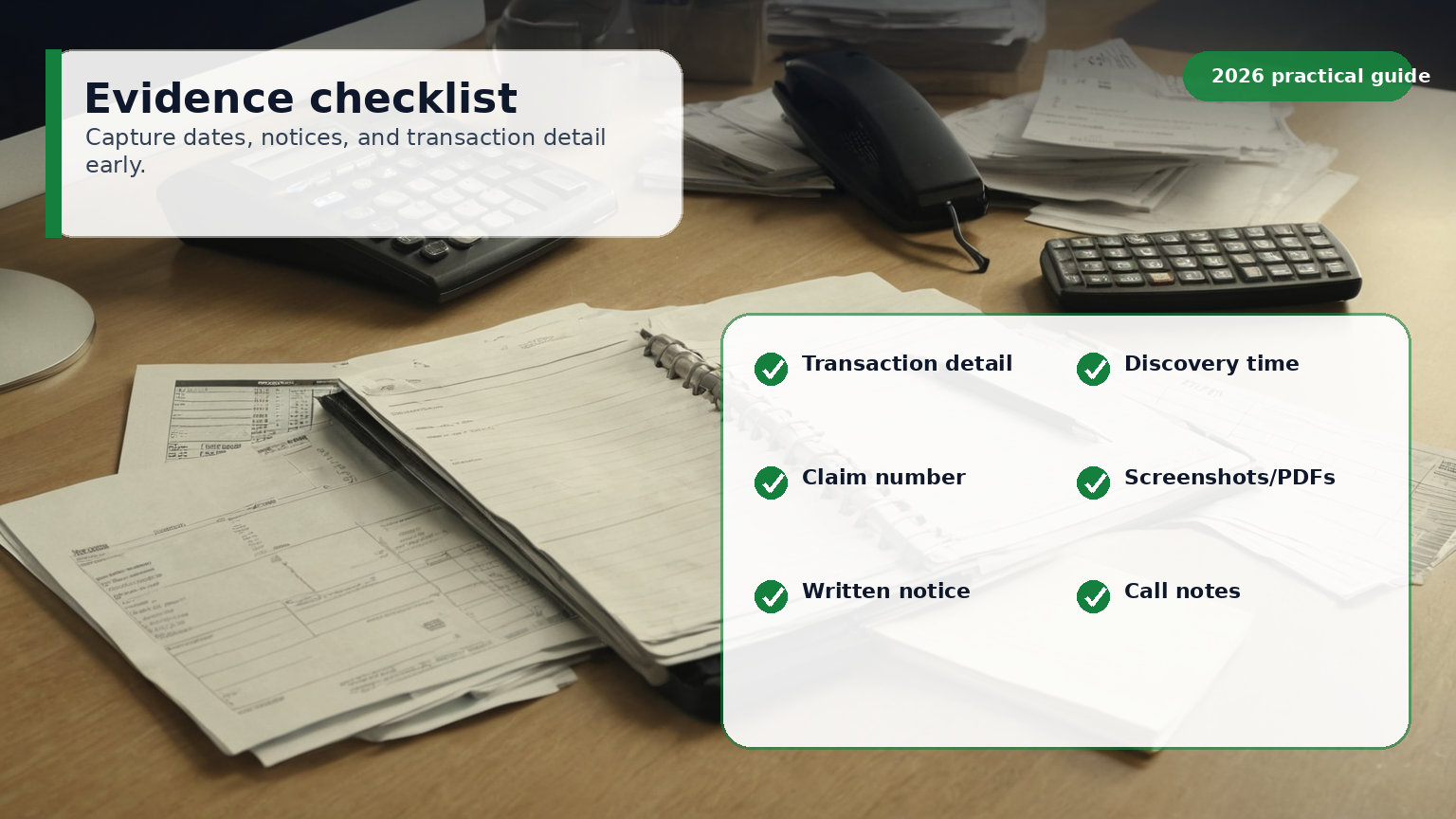

The practical move is to sort the event before calling it by a legal label. Write down the account, date posted, transaction description, amount, channel, and why you believe it was unauthorized or erroneous. If several transactions occurred, list each line separately. Banks often investigate transaction by transaction, so a clean list beats a long emotional paragraph.

| Situation | Likely first path | Cash-flow caution |

|---|---|---|

| Debit-card charge you did not make | Bank Regulation E dispute and card replacement | Freeze the card, but verify pending legitimate bills that used it. |

| ACH pull from your checking account | Bank dispute, originator block, written stop-payment request | Move bill money to a clean account if account numbers are exposed. |

| ATM withdrawal you did not make | Bank fraud claim, PIN/card compromise review | Ask how to access cash while the card is replaced. |

| You sent money after a scam message | Contact bank/payment app immediately and report to FTC | Recovery may be harder; build a replacement-cash plan immediately. |

| Credit-card charge dispute | Credit-card billing dispute rules, not this checking-account playbook | Do not drain checking to pay a disputed credit charge without reviewing options. |

The first hour: stop the leak before optimizing the claim

The first hour is about containment. Lock the debit card in the app if available, change the banking password from a trusted device, enable multi-factor authentication, and call the bank using the phone number on the card or official website. If the account number itself may be compromised through an ACH pull, ask whether the bank can block the originator, restrict electronic debits, or open a replacement account. Do not click a phone number inside the suspicious text or email that started the event.

At the same time, preserve evidence. Take screenshots of the transaction detail page, pending transactions, alerts, text messages, emails, device login notices, and any chat with a merchant or payment app. Export statements if possible. If you later file a CFPB complaint, FTC report, police report, or appeal, the dates will matter more than your memory.

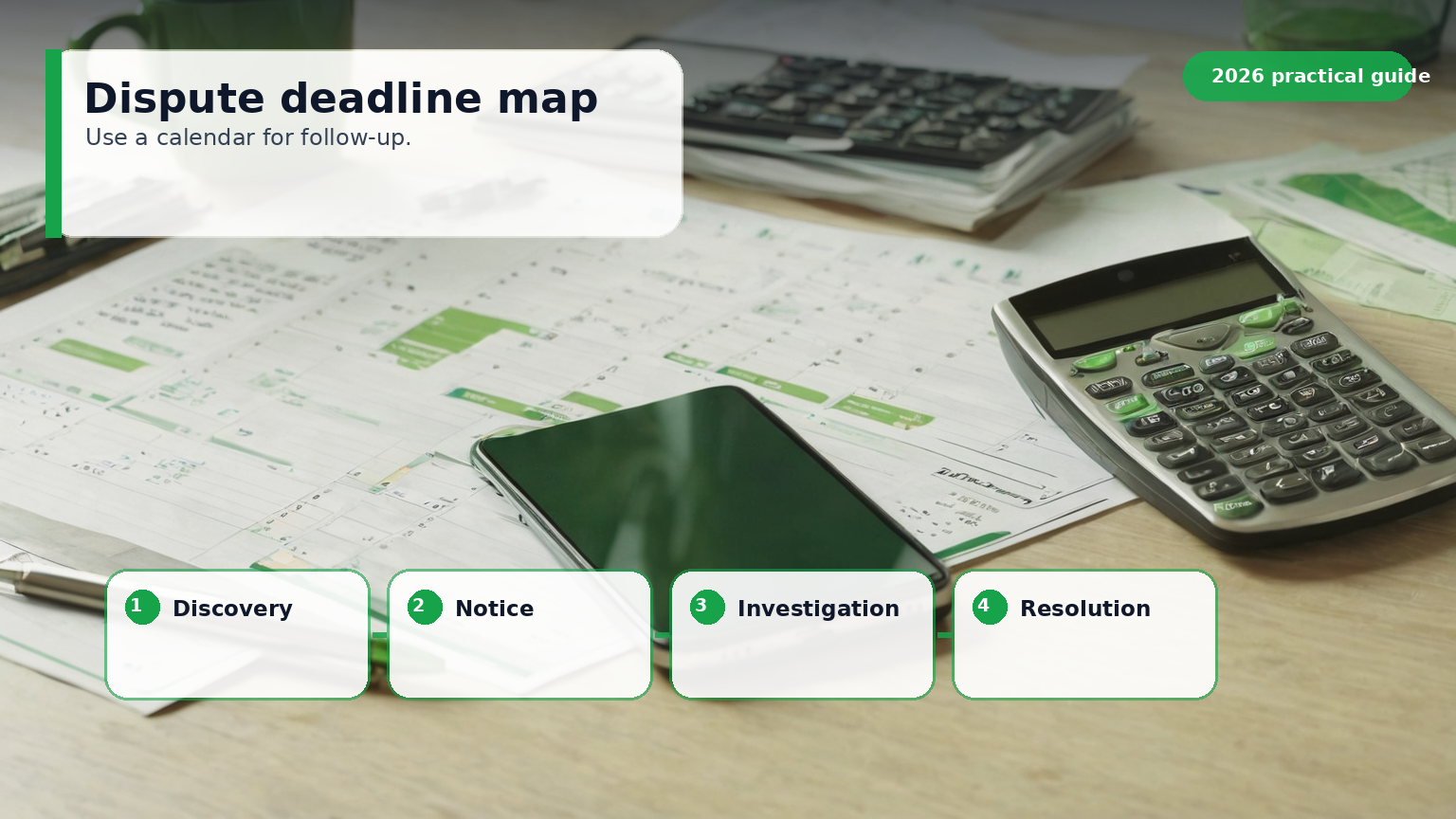

The deadline map: why prompt notice matters

Regulation E has timing rules for consumer notice, institutional investigation, provisional credit, and final explanations. The exact result depends on facts, account type, and transaction type, so do not rely on a generic social-media deadline chart as legal advice. Still, the pattern is important: prompt notice helps preserve rights, and written follow-up reduces confusion.

A useful workflow is: call immediately, ask for the claim number, then send a short written dispute through the bank’s secure message center, branch, fax, or mailing address the bank specifies for disputes. The written note should identify the transactions, state that you did not authorize them or that an error occurred, include the date you discovered the problem, and request investigation under applicable electronic-fund-transfer rules. Keep a copy.

The cash-flow lesson is conservative: do not spend provisional credit as if it is permanent. Provisional credit can keep the household running during an investigation, but it may be reversed after a final decision. Label it in your budget as disputed money until the bank confirms the claim is resolved in your favor.

Build a temporary cash-control system

Fraud often exposes an account-design problem. If one checking account holds rent, groceries, emergency savings, subscriptions, and debit-card spending, one compromise can disrupt everything. After the immediate report, separate cash into safer buckets.

Start with a daily-spending account that carries a deliberately low balance. Then keep a bill-pay account for rent, utilities, insurance, and debt minimums. Keep emergency savings at a separate institution or at least in a separate savings account without a debit card. If your main checking account must be closed, this separation can prevent every biller from failing at once.

If a paycheck is arriving soon, redirect direct deposit only through trusted employer or payroll portals. If autopay is attached to the compromised account, prioritize essential bills first: housing, utilities, insurance, minimum debt payments, childcare, and transportation. Contact billers before due dates and document any fee-waiver requests. The FDIC’s consumer information on overdraft and account fees is a reminder that a fraud event can create secondary costs even after the original transaction is investigated.

Dispute language that stays useful

A dispute does not need legalese. It needs clarity. A strong message might say: “I am disputing unauthorized electronic fund transfers from my consumer checking account. I discovered the activity on May 25, 2026. The transactions are: [date, merchant/originator, amount]. I did not authorize these transfers and request investigation, provisional credit if required, written results, and copies of documents relied on if the claim is denied. Please confirm the claim number and mailing or secure-message address for additional documents.”

Avoid overclaiming facts you cannot prove. For example, do not say your identity was stolen if you only know that one transaction is unfamiliar. Instead, say what you know: the transaction is unauthorized, the card is in your possession or not, you did not share credentials, a phishing text arrived, or a device was lost. Clean facts help the investigator classify the claim.

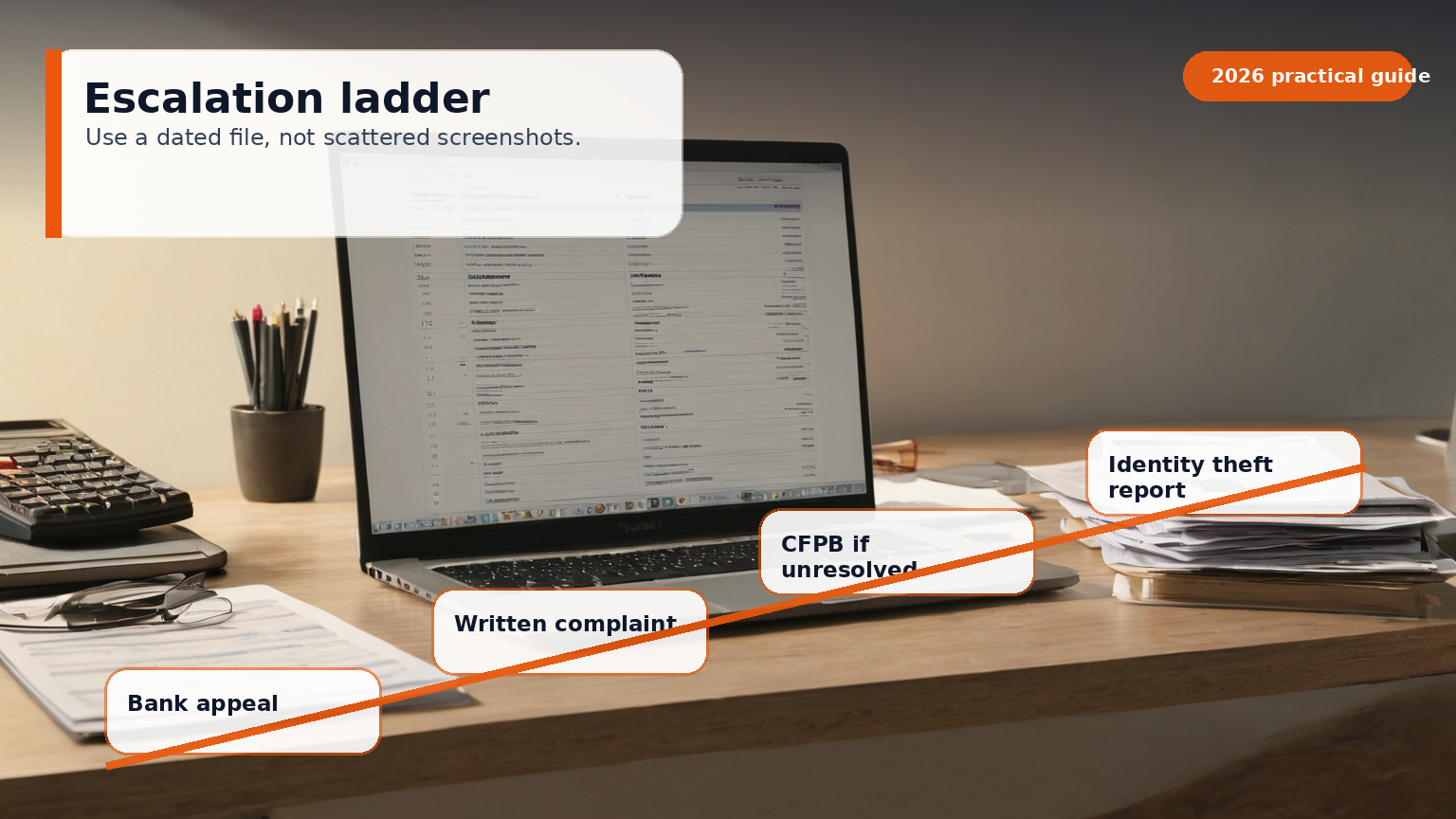

When the bank denies or delays the claim

If the bank denies the claim, ask for the written explanation and the evidence it relied on. Compare that explanation with your records. Did the bank confuse an authorized merchant subscription with a new unauthorized debit? Did it decide the transaction used your device, while you have evidence that your phone was replaced or your login was compromised? Did it ignore a written notice or a police report?

Escalation works best when it is structured. First, appeal within the bank using the claim number and new facts. Second, consider a CFPB complaint for consumer financial products and services. Third, report scams or identity theft to the FTC, especially if personal information was misused. For identity theft, the FTC’s identity-theft resources can help create a recovery record. If the loss is large, involves elder exploitation, or includes threats, contact local law enforcement or a qualified attorney.

Prevent the next cash-flow crisis

After the dispute is stable, harden the account. Replace the debit card, update passwords, remove unused payment apps, revoke old merchant authorizations, and turn on transaction alerts for card-not-present purchases, ATM withdrawals, ACH debits, and low balances. Consider keeping debit cards away from routine online shopping and using a credit card for purchases where appropriate, because credit cards generally separate merchant disputes from the checking account that pays rent.

Review bank account connections inside budgeting apps, tax software, payroll tools, and peer-to-peer payment apps. Many people close the visible card but forget a connected service that still has account access. If an account number was exposed, ask the bank whether a new account is safer than repeated blocks. Keep a small printed or offline list of critical billers so you can rebuild autopay quickly without searching through a compromised inbox.

A conservative household action plan

Use this seven-step order when cash is tight:

- Freeze the card or account access and call the bank from an official number.

- List each disputed transaction separately with date, amount, and description.

- Send written notice and save the claim number.

- Move undisputed cash for rent, utilities, insurance, food, and transportation.

- Treat provisional credit as disputed, not spendable surplus.

- File FTC, police, or CFPB reports when the facts support escalation.

- Rebuild account buckets so one compromised payment rail cannot drain everything.

The goal is not to become a banking-law expert overnight. The goal is to preserve rights, protect essential bills, and keep enough documentation that the next reviewer can understand the case quickly.

Sources and further reading

- Electronic Fund Transfers, 12 CFR Part 1005 (Regulation E) — eCFR.

- What should I do if there are unauthorized transfers from my bank account? — CFPB.

- How do I stop automatic payments from my bank account? — CFPB.

- What To Do if You Were Scammed — FTC Consumer Advice.

- Identity Theft and Phishing Scams — FTC.

- Overdraft and Account Fees — FDIC.

- Regulation CC: Availability of Funds and Collection of Checks — Federal Reserve Board.